Global oil reserves are falling due to the closure of the Strait of Hormuz. Several buffers have prevented oil prices from soaring. Oil is in a race

- Global oil reserves are falling due to the closure of the Strait of Hormuz.

- Several buffers have prevented oil prices from soaring.

Oil is in a race against time. The longer the Strait of Hormuz remains blocked, the greater the chances of higher Brent and WTI prices in the longer term. The US Energy Information Administration estimates a reduction in global oil reserves of 2.6 mln bpd, assuming the world’s main artery resumes operations by summer. This figure is significantly higher than the previous forecast of 0.3 mln bpd. The average price of North Sea crude in 2026 is expected to be $95 per barrel.

The International Energy Agency estimates the oil market deficit at 1.78 mln bpd. In April and December, it forecast surpluses of 0.41 mln bpd and 4 mln bpd, respectively. Even if the conflict in the Middle East ends by early June, a serious imbalance will persist until the end of the third quarter.

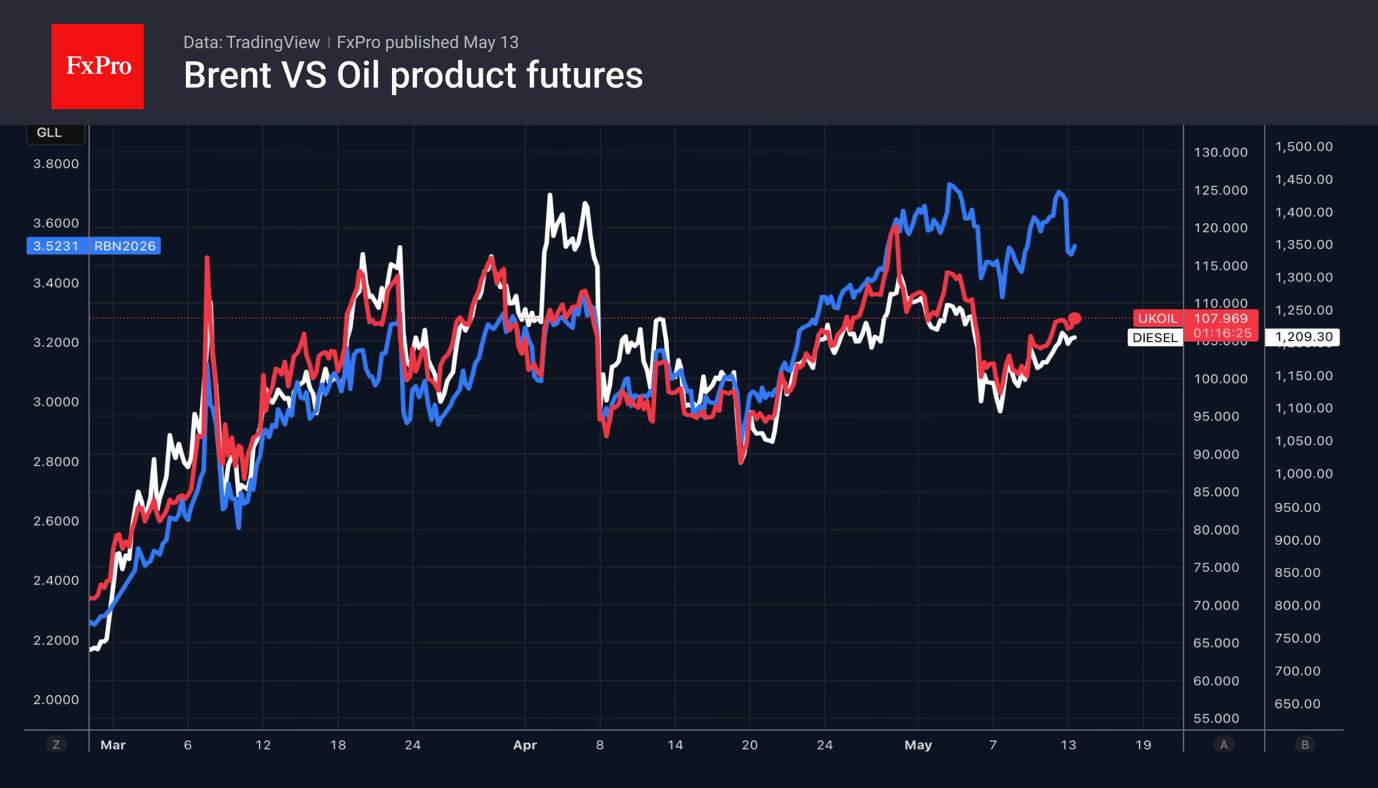

Given these figures, the price of a barrel of Brent at around $105 seems too low, as it has hovered near this level since the second half of March. Moreover, there is now almost no difference between futures and spot prices, whereas at the start of April, the spread exceeded $30, a record high. What is the reason for this?

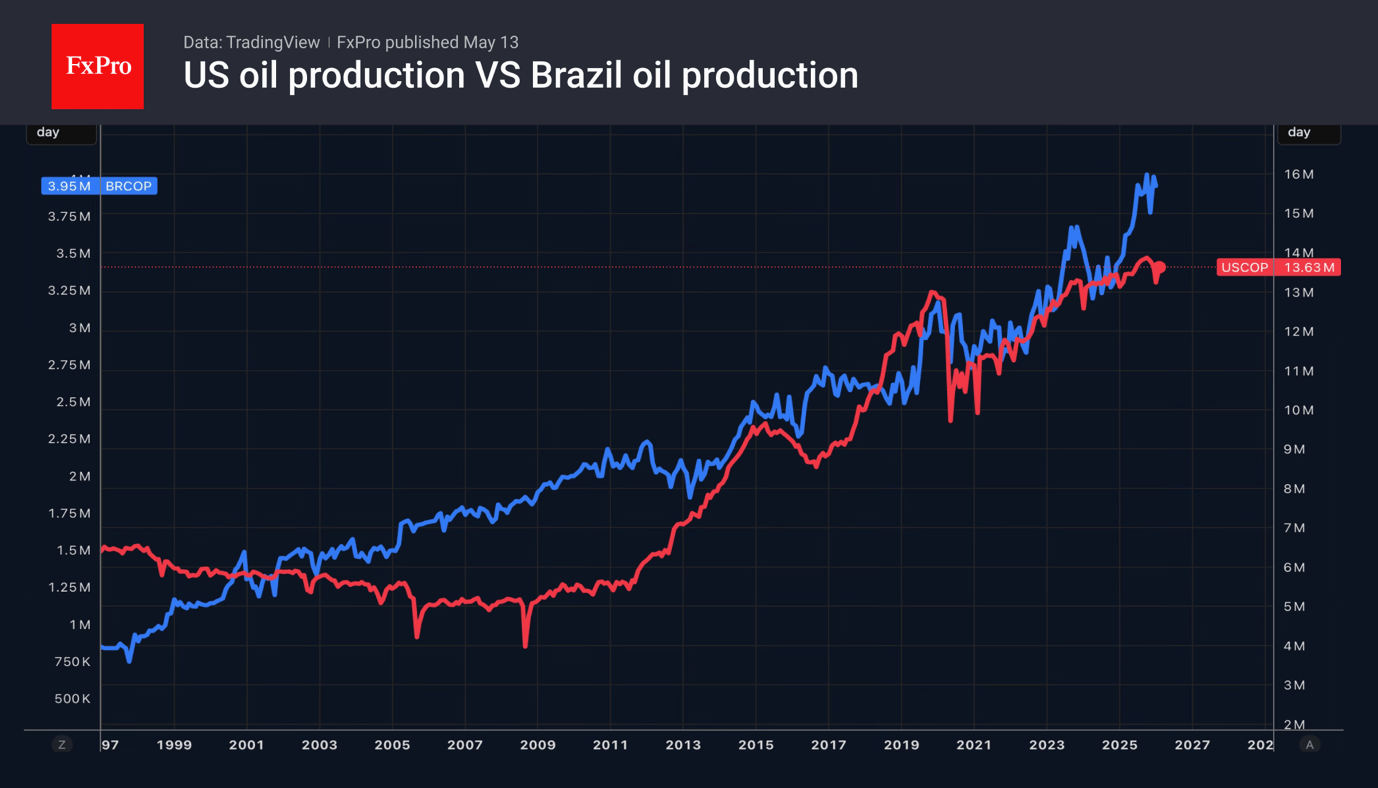

The global oil market has managed to utilise several buffers that are currently holding back price rises. Before the conflict in the Middle East, it was in surplus, building stocks and bringing China’s reserves to an impressive 1.4 bn barrels—more than a year’s consumption. The US is exporting nearly 10 mln bpd, compared with 4–6 mln bpd in the previous couple of years. Canada has increased exports by 0.4 mln bpd compared with a year earlier; Venezuela and Norway by 0.2 mln each; and Brazil by 0.1 mln. Saudi Arabia and the UAE have also found workarounds.

JP Morgan points to faster growth in petrol and diesel prices compared with crude oil. This reduces consumer demand and decreases refineries’ need for feedstock. The US Energy Information Administration forecasts a slower increase in global demand in 2026—from +0.6 mln bpd in the previous estimate to +0.2 mln bpd. Furthermore, calculations indicate a drop in demand of approximately 5 mln bpd. This is too significant to be considered a sustainable trend, signalling that consumers are simply trying to weather the storm, whereas in 2022, they were rushing to stock up. It is worth noting separately that some of the lost demand may not return to the market at all, reviving interest in alternative energy sources.

Nevertheless, the oil shortage created by the closure of the Strait of Hormuz is laying the foundations for future price growth. The blockade of the world’s key oil artery is leading to overflowing storage tanks, reduced production, and destroyed capacity. Thus, time is on the side of the Brent bulls.

SOURCE LINK : Time Is on Crude’s Side